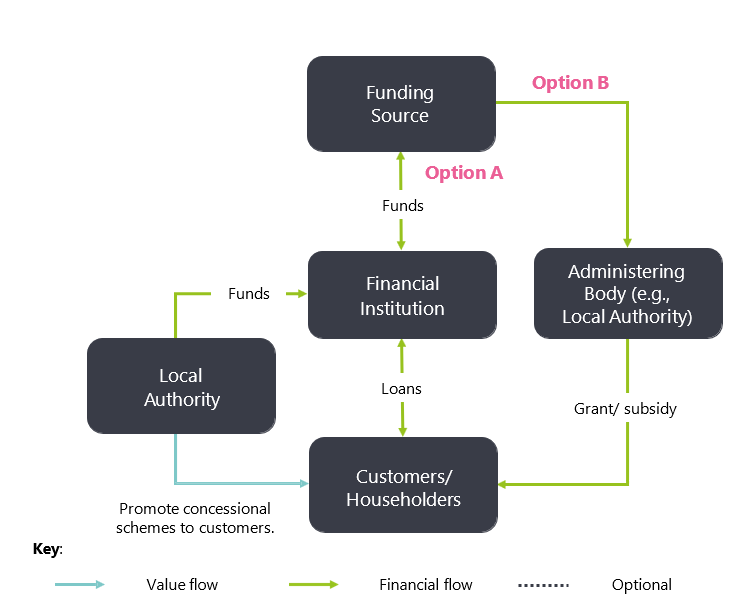

Concessional finance offers customers more favourable financing terms than those available in the open market, such as lower interest rates, extended repayment periods, grace periods, and/or percentage grants.

Resource

Concessional finance offers customers more favourable financing terms than those available in the open market, such as lower interest rates, extended repayment periods, grace periods, and/or percentage grants.

Experience Level:

Smart ClientProvided by: Energy Systems Catapult

It is typically provided for projects/technologies that demonstrate positive environmental impacts.

Concessional finance can be offered to customers in various forms:

- Option A: A concessional loan provided by a financial institution.

- Option B: A grant awarded directly from a funding source (e.g., central government) and distributed by an administering body.

Local authorities could support or enable concessional finance in several ways:

- Partnering with a financial institution to promote concessional schemes through their existing channels.

- Administering grants on behalf of central government to eligible consumers.

- Providing capital to a financial institution, seeking only the return of the original funds rather than a profit, thereby ensuring an affordable interest rate for customers.

The Home Energy Scotland Grant and Loan Scheme, funded by the Scottish Government, offers homeowners in Scotland financial support in the form of grants, interest free loans or a combination of both to install clean heating systems and energy efficiency measures.

For clean heating systems (e.g., heat pumps), homeowners can receive a grant of up to £7,500, with an additional optional interest-free loan of up to £7,500.

For energy efficiency measures (e.g., insulation), grant funding is available for up to 75% of the combined cost of measures. This is capped at a maximum amount of £7,500. The remainder of funding required can be taken up as an optional interest-free loan (up to the maximum funding limit per improvement – see Home Energy Scotland. (2025) below for further information on the maximum funding limit for each specific improvement, measure, or technology).

Rural and island homes are eligible for an additional £1,500 uplift applied to both clean heating and energy efficiency grants, bringing the maximum available grant funding to £18,000.

Home Energy Scotland provides advisory services for potential applicants, while the scheme is administered by the Energy Saving Trust, an organisation accredited by the Financial Conduct Authority.

Householders can choose how long to take to repay the loan, subject to maximum terms based on the borrowed amount:

In the financial year 2023-2024, the scheme had a budget of £56 million, with £54,080,923 distributed by the end of Q3.

Lendology provides loans funded by local partner councils to address specific community needs. Lendology recently partnered with Suffolk County Council to launch the £3 million Warm Homes Suffolk loan.

The interest-free loan scheme helps homeowners invest in energy-efficient upgrades such as insulation, solar panels, battery storage, glazing, and heat pumps. The £3 million funding was secured as part of the council’s ‘County Deal’ negotiations and is targeted at residents who do not qualify for other grants.

The scheme is designed to be self-sustaining, with loan repayments reinvested to support future applicants.

Homeowners can borrow up to £15,000 at 0% interest (0.2% representative APR). Loan terms span up to seven years, with no early repayment charges.

A £20 fee is required to register a Title Restriction against the property, meaning the home cannot be sold without approval unless the loan is fully repaid.

Beyond the Warm Homes Suffolk loan, as of 2022, Lendology had issued 2,856 loans, totalling £16,876,523. Of this total, £9,851,326 had been recycled back into the fund.

Loan repayment rates remain strong, with less than 0.2% (£29,000) outstanding.

ESC is making this report available under the following conditions. This is intended to make the Information contained in this report available on a similar basis as under the Open Government Licence, but it is not Crown Copyright: it is owned by ESC. Under such licence, ESC is able to make the Information available under the terms of this licence. You are encouraged to Use and re-Use the Information that is available under this ESC licence freely and flexibly, with only a few conditions. Using information under this ESC licence Use by You of the Information indicates your acceptance of the terms and conditions below. ESC grants You a licence to Use the Information subject to the conditions below. You are free to:

You must, where You do any of the above:

These are important conditions of this licence and if You fail to comply with them the rights granted to You under this licence, or any similar licence granted by ESC, will end automatically.

Designed to aid Local Authorities in developing robust, evidence-based plans to enable Net Zero.

Already have an account? Login

Guest preview of selected publicly available resourcesFull library of 1,000+ articlesCPD accredited e-learning coursesCase studiesDiscussion forum

Guest preview of selected publicly available resourcesFull library of 1,000+ articlesCPD accredited e-learning coursesCase studiesDiscussion forum