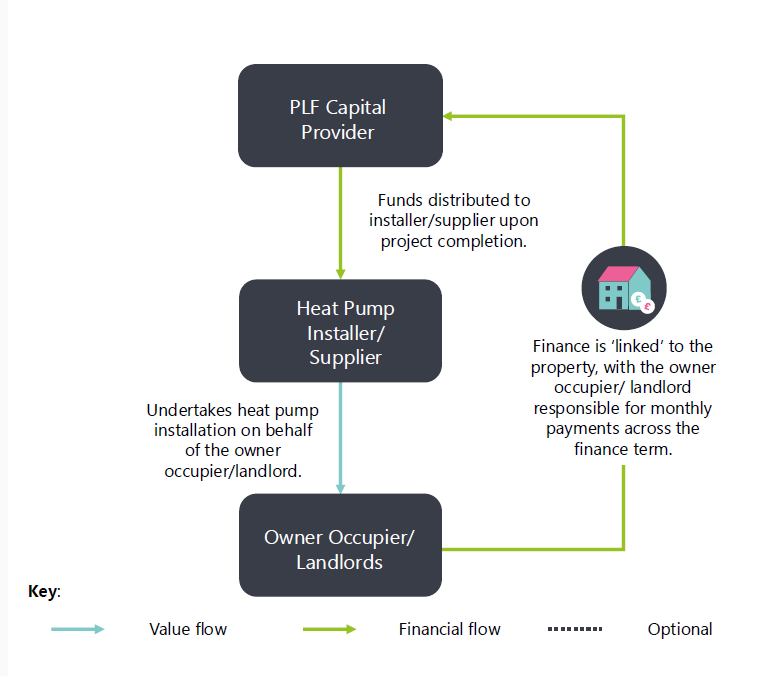

Property-linked finance (PLF) is a financial mechanism where loans are attached to a property rather than an individual or business.

Resource

Net Zero Go will be down for scheduled maintenance: Wednesday 5th August 09:00-12:00

Property-linked finance (PLF) is a financial mechanism where loans are attached to a property rather than an individual or business.

Experience Level:

Smart ClientProvided by: Energy Systems Catapult

It can support the decarbonisation of properties by funding low-carbon technologies and/or interventions such as heat pumps, solar PV, energy storage, and energy efficiency improvements.

When the property is sold, the repayment obligation transfers to the new owner(s), ensuring the loan remains tied to the property.

There are several ways that PLF could be delivered:

- Option A: Private sector financing – Private sector capital providers fund building decarbonisation projects and establish a property-linked finance agreement, using a suitable linking mechanism.

- Option B: Local authority financing – Local authorities act as capital providers and recover payments through Council Tax.

- Option C: Utility financing – A utility company provides financing and collects repayments via utility bills.

PLF is not currently available in the UK but has been demonstrated in other countries such as the United States and Australia. The concept is also being explored by authorities in the UK, including the Greater Manchester Combined Authority and the West Midlands Combined Authority.

In collaboration with Lloyds Banking Group and Natwest Group, the Green Finance Institute has proposed a ‘greenprint’ for how PLF could be introduced, executed and scaled. The approach is based on five guiding principles:

The partnership also explored what mechanisms could enable the linking of finance to properties so that the payment obligations run with the land. For residential PLF, ‘Local Land Charges’ emerged as the most aligned linking mechanism. These are financial charges or restrictions on the use of land.

Local authorities are responsible for maintaining the Local Land Charges register for their areas, though this responsibility may be transferred to the Land Registry.

The greenprint also highlighted several key questions for future research:

ESC is making this report available under the following conditions. This is intended to make the Information contained in this report available on a similar basis as under the Open Government Licence, but it is not Crown Copyright: it is owned by ESC. Under such licence, ESC is able to make the Information available under the terms of this licence. You are encouraged to Use and re-Use the Information that is available under this ESC licence freely and flexibly, with only a few conditions. Using information under this ESC licence Use by You of the Information indicates your acceptance of the terms and conditions below. ESC grants You a licence to Use the Information subject to the conditions below. You are free to:

You must, where You do any of the above:

These are important conditions of this licence and if You fail to comply with them the rights granted to You under this licence, or any similar licence granted by ESC, will end automatically.

Designed to aid Local Authorities in developing robust, evidence-based plans to enable Net Zero.

Already have an account? Login

Guest preview of selected publicly available resourcesFull library of 1,000+ articlesCPD accredited e-learning coursesCase studiesDiscussion forum

Guest preview of selected publicly available resourcesFull library of 1,000+ articlesCPD accredited e-learning coursesCase studiesDiscussion forum